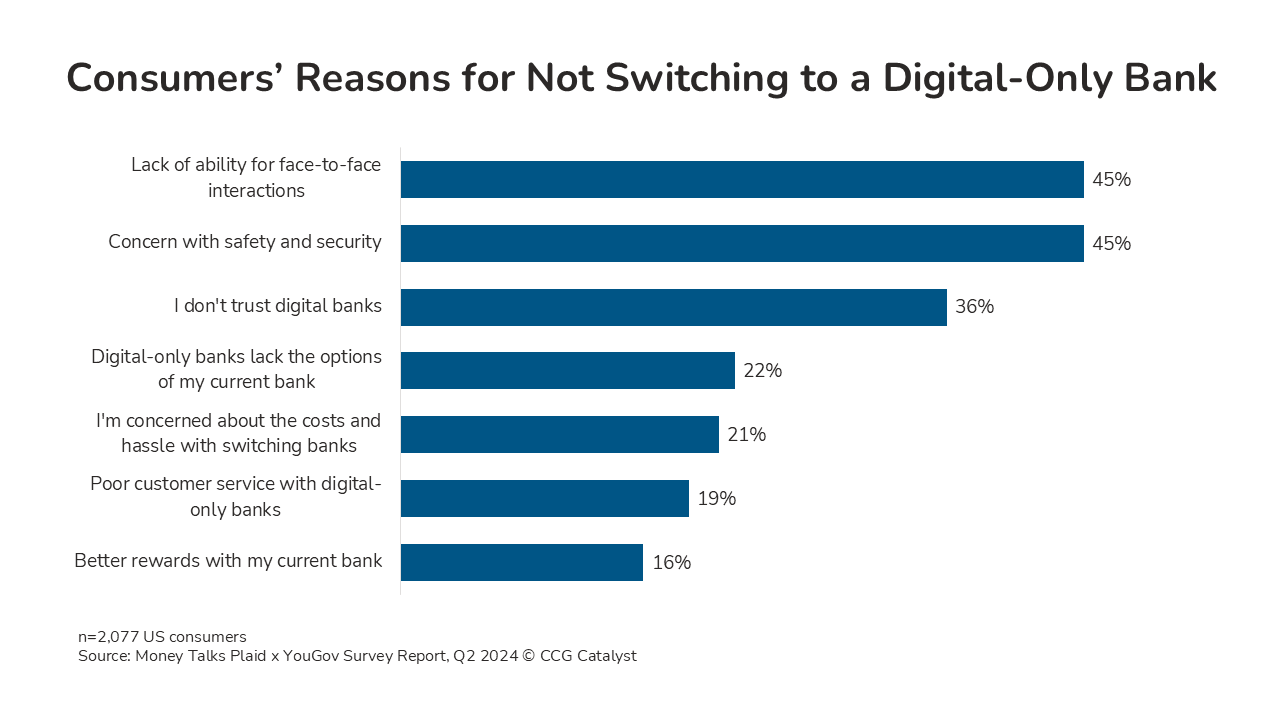

One of the top two factors that stop traditional bank customers from moving to digital-only banks is the lack of ability for face-to-face interactions, according to a study from Plaid and YouGov. While consumers overwhelmingly favor banking via digital channels, elements of branch banking may still be a competitive advantage for traditional financial institutions (FIs). A persistent challenge for traditional banks, however, is the cost structure of branch banking and their ability to offset those costs.

Within the survey’s context, FIs have two overlapping options: 1) Diligently manage the operating costs of face-to-face interactions and 2) subsidize the cost of face-to-face interactions with sales that digital-only competitors won’t offer or can’t offer effectively.

Here are a couple of ways we think these actions could play out:

FIs may close or modify branches and adapt the roles of branch staff to better reflect customer interactions with the highest return. They may also invest in digital banking features that reduce or eliminate the need for a physical branch for some face-to-face services and encourage the digitization of front-office and administrative processes that are paper-based in the branch. FIs may particularly benefit from how the pandemic normalized video conferencing for face-to-face interactions and made it an accepted alternative to in-person meetings.

FIs can use face-to-face channels to support fee-generating businesses, like financial advice, and expedite the sale and closing processes for highly profitable products that contribute to net interest margin. Using face-to-face channels to retain customers for their deposits alone may not be worth the expense of servicing those customers.

A face-to-face strategy that combines cost efficiency and maximizing sales of the most profitable products and services is crucial when traditional banks must compete with digital-only competitors for customers. They must maintain digital self-service that is robust enough to handle a wide range of customer needs when face-to-face interactions aren’t warranted or practical. (That includes, for example, 24/7 customer service; the survey suggests that many consumers value it).

Bankers may feel stuck between a rock and a hard place. Does doing everything their competitors do make FIs more competitive? Not necessarily. It’s easy to mistake the ability to do something for its business value and make or stick to a decision that no longer makes sense.

FIs should keep in mind the following when they consider their strategy for face-to-face customer interactions:

Face-to-face interactions differentiate traditional FIs when they preserve customer trust, meet customer service expectations, and are delivered at a reasonable cost.

The sale of high-value products and services should be part of face-to-face services while lower-value interactions that justify little overhead are digitized.

Competing with digital-only banks should be about making disciplined choices about where in-person service differentiates the FI’s value to customers.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.