A Framework for Evaluating Fintech

SEPTEMBER 26, 2024

By: Tyler Brown

Bank Partnership Strategy

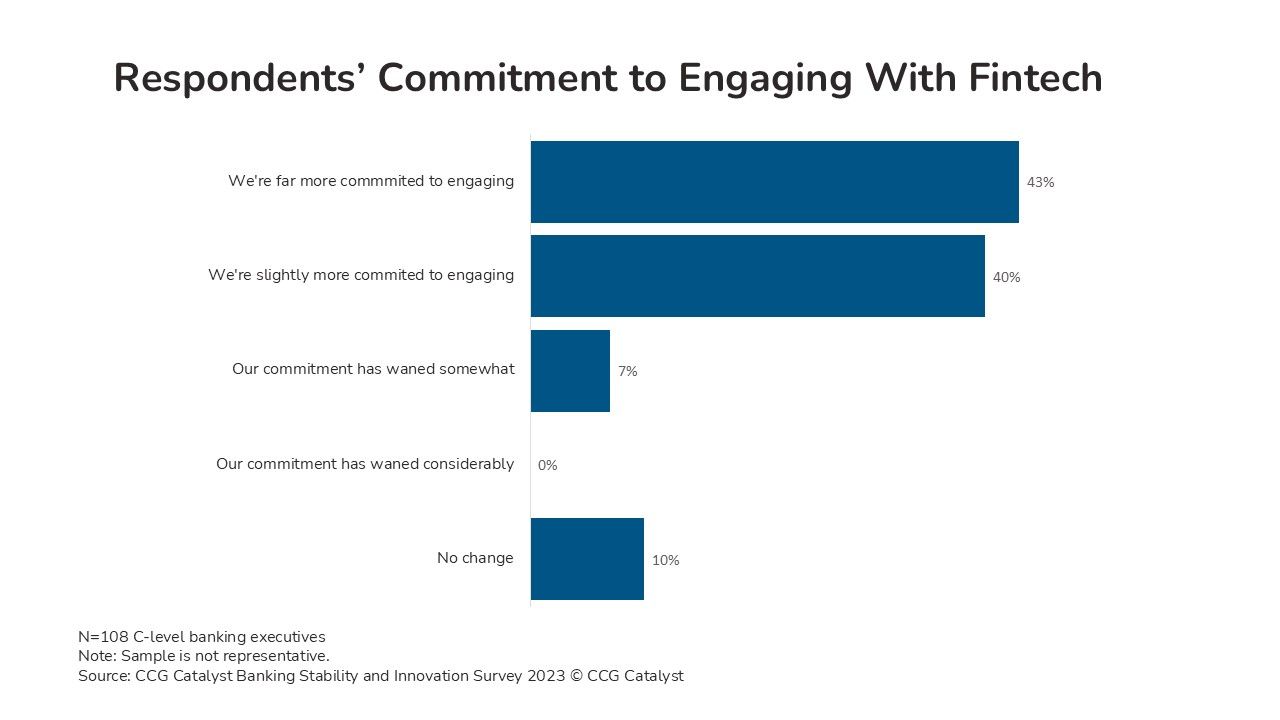

In CCG Catalyst’s Banking Stability and Innovation Survey 2023, respondents leaned into plans to work with the fintech industry: 83% said that in the last 12-18 months they became slightly or far more committed to engaging with it. Respondents’ intents bode well for the partnership-driven future of banking technology and their financial institutions’ (FIs’) modernization. But that mindset forms only the basis of a strong fintech strategy.

To be actionable, bankers’ definition of “fintech” should be complete and specific. Popular fintech conjures images of third-party distributors of banking services — consumer payment apps and neobanks — and other companies that facilitate customer-facing depository and payments products. But those are only the tip of the iceberg. Business-focused and enterprise fintech dovetail with enabling technology for FIs, including applications that are tailored to financial services but aren’t tied directly to products.

Bankers’ concept of fintech needs a framework that accounts for all the above, incorporating 1) financial products, 2) enterprise technology, and 3) channels.

Financial products

Financial products put the “fin” in “fintech.” In this category, technology emphasizes deposits, lending, or payments, and can be placed in the front, middle, or back office. And when an end customer interacts with a product, it will typically be through an FI’s direct channels. The “deposits” category, for example, may include recordkeeping and treasury management or deposit networks; “lending” may include origination, decisioning, compliance, or portfolio analytics; “payments” may include rails or payment network integration and routing technology.

Embedded-finance enablers, also known as BaaS platforms, also sit in this category because they enable the distribution of a bank’s products and services. The industry’s pivot to selling technology directly to FIs keeps it in this box as these enablers take on roles that can make them look a lot like side cores, but bundle bank tech products that may be tuned to work with third-party channels.

Enterprise technology

Enterprise technology covers software applications with use cases in banking that serve critical functions but don’t apply directly to products. The category divides roughly into operations and risk, fraud, and compliance. There’s a lot going on in the latter group with identity management, biometrics, compliance testing and reporting, and cyber risk management.

Channels

“Channels” fintechs are front-end distributors of banking products that generate revenue for FI partners. This category covers Banking-as-a-Service (BaaS) channel partners, known once almost exclusively as neobanks. With the growth of embedded finance and the lines blurring between financial products and Software-as-a-Service (SaaS) or commerce solutions, this category is branching off from fintech. It’s “fintech-enabled” via infrastructure that serves the distributor, the BaaS sponsor bank, or both. Front-end pure fintech is harder to find as solutions are bundled.

What it means to engage

A vague commitment isn’t enough to make a fintech strategy work. FIs’ engagement with fintech comes in several overlapping flavors: Bank tech partnerships, channel partnerships, and strategic investments (which may be pooled or direct). The path an FI chooses should be unique to its capabilities and business direction. But the need for board commitment to a fintech strategy and management buy-in to a clear direction are universal.