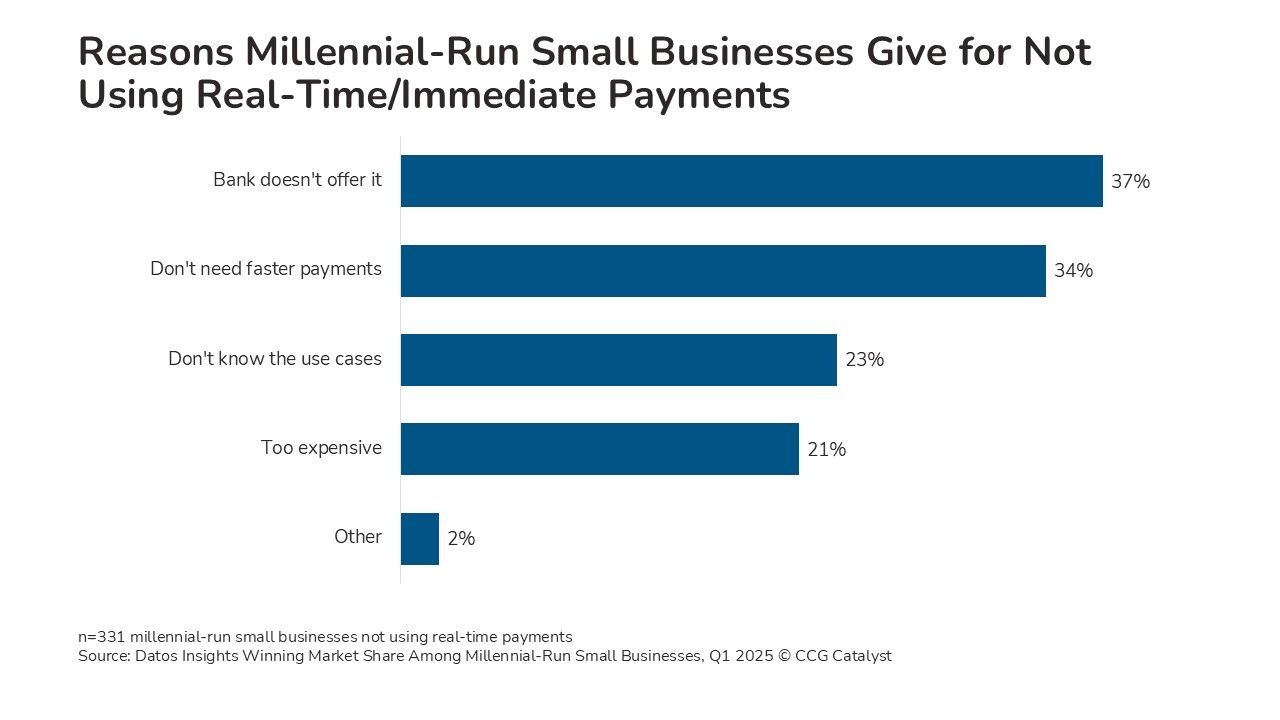

Seventy-two percent of millennial-run small businesses don’t use real-time payments, instead leveraging business credit and debit cards, PayPal, and ACH, according to a Datos survey. The top reason why a company doesn’t use real-time payments is their bank doesn’t offer it. Outside of a lack of need, this is followed by not enough knowledge about how real-time payments can be used, then cost. Availability, lack of understanding, and cost add up to 81% of the respondents who don’t use real-time payments.

With FedNow live at 1,405 financial institutions (FIs) and RTP live at 965, a critical mass of FIs may be able to offer small-business customers real-time payments. The millennial cohort is especially important as they age and increasingly start their own businesses. With a full suite of real-time payments functionality, including send, receive, and request for payment, small businesses may increase their working capital by having customer payments settle instantly and paying vendors and employees “just in time.”

The three hurdles to these businesses’ adoption of real-time payments — availability, customer education, and cost — are all issues a bank can solve:

Availability is a business and technology decision for the bank. The business decision is to ask which payment methods small businesses are using now, and which ones have or may have the greatest benefit to the FI’s bottom line in the long run. The benefit may be based on processing revenue, revenue from payments-adjacent products and services, and total relationship value with its small-business customers. For the bank, key considerations are also the upfront costs and operating expenses related to a real-time payments option.

Education about the use cases for real-time payments is incumbent partly on small businesses themselves when they think about their payment needs and partly on relationship managers at their bank. Small-business owners need to know what real-time payments are for and that they’re available. The bank’s motivation to educate their small business customers will come when real-time payments are ultimately a profit-driver for the relationship.

Cost is a product of the expenses a bank passes through to its customers, what it charges for processing and value-added services, and which products and services customers buy that may subsidize real-time payments. For example, the bank can take a loss on real-time payments in the interest of capturing deposits and selling small-business loans or design real-time payments as a revenue source. It is the bank’s choice whether real-time payments are “too expensive” for small-business customers after startup costs are accounted for.

Banks should ask themselves how real-time payments can enhance small-business relationships, especially when it comes to younger owners who may be inclined to appreciate the efficiency, given how their expectations have been conditioned elsewhere. Banks should start by articulating clear business use cases for real-time payments, like accelerating the settlement of accounts receivable or eliminating negative float for vendor payouts and payroll. For banks, real-time payments offered to businesses present opportunities to grow deposits, support the delivery of new cash management products, and cross-sell business lending.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.