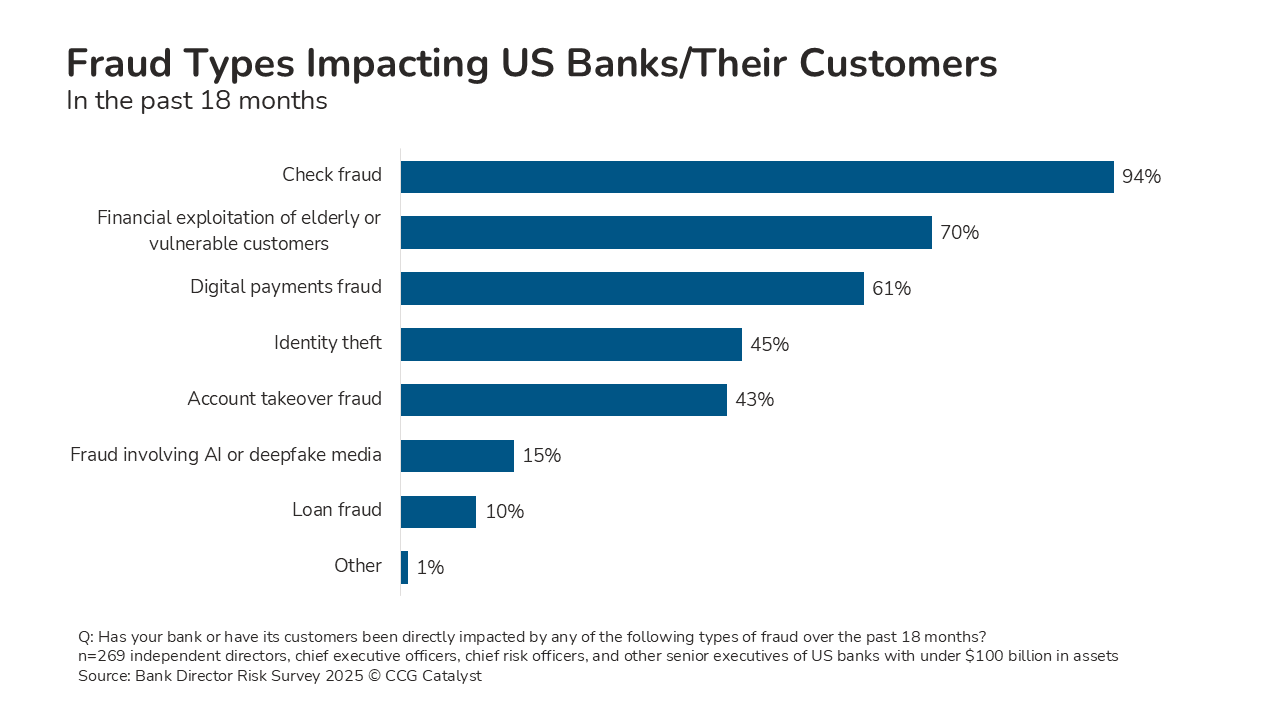

Ninety-four percent of bank executives who responded to a survey by Bank Director said their bank or its customers had been directly impacted by check fraud over the past 18 months. This points to weaknesses in a legacy payment method that still has substantial transaction volume: The Fed processed nearly 3 billion checks in 2024, even as the number declined. In the meantime, financial institutions (FIs) in a Fed survey reported that their fraud losses due to counterfeit checks, check washing, and payee forgery rose.

Checks written by both businesses and consumers are targets for fraud — 73% of businesses that responded to a Fed survey said they used checks in the last 12 months, and in another Fed survey, 35% of consumers said they used checks in the last 30 days (they averaged 1.2 checks per month). FIs may be less exposed to check-related losses than for card payments (consumer electronic funds transfer protections don’t apply), but they face expenses related to fraud investigation and voluntarily paying claims. The important thing is ensuring that fraud losses are in line with the bank’s tolerance limits.

Some solutions to check fraud overlap: A natural way to reduce check fraud is to reduce the volume of checks written, for example, by not offering paper checks with certain accounts; the corollary is to offer attractive alternatives like electronic P2P payments. Customer migration to real-time payments, which are by design incompatible with paper checks, may also help resolve the issue.

Additionally, banks can implement more sophisticated systems that increase the reliability of straight-through check processing and expedite fraud analysts’ ability to make decisions that a machine can’t within an FI’s risk tolerance. Given federal rules on check processing and funds availability, faster detection and response to check fraud is crucial. This may include continuous investment in modern resources, rather than relying on outdated check-fraud systems.

Importantly, none of these options should exist in isolation; they must come together under a cohesive fraud management strategy. That strategy should extend beyond any one kind of fraud, especially as activity will inevitably shift as institutions more effectively combat check fraud and payment volumes rise on other rails. Bank accounts are vulnerable to ACH pull-payment fraud (due to stolen account information), unauthorized push payment fraud (due to stolen credentials), and authorized push payment fraud (due to social engineering).

As such, it is important to think holistically about how to keep fraud under control on different fronts, so that institutions don’t end up playing whack-a-mole. That requires staying vigilant, keeping up with threats, and regularly revisiting the weakness and protections inherent in their payment offerings and supporting technology.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.