How AI Can Speed Bank Onboarding — And Reduce Abandonment

How AI Can Speed Bank Onboarding — And Reduce Abandonment

March 21, 2024

By: Tyler Brown

AI and Onboarding

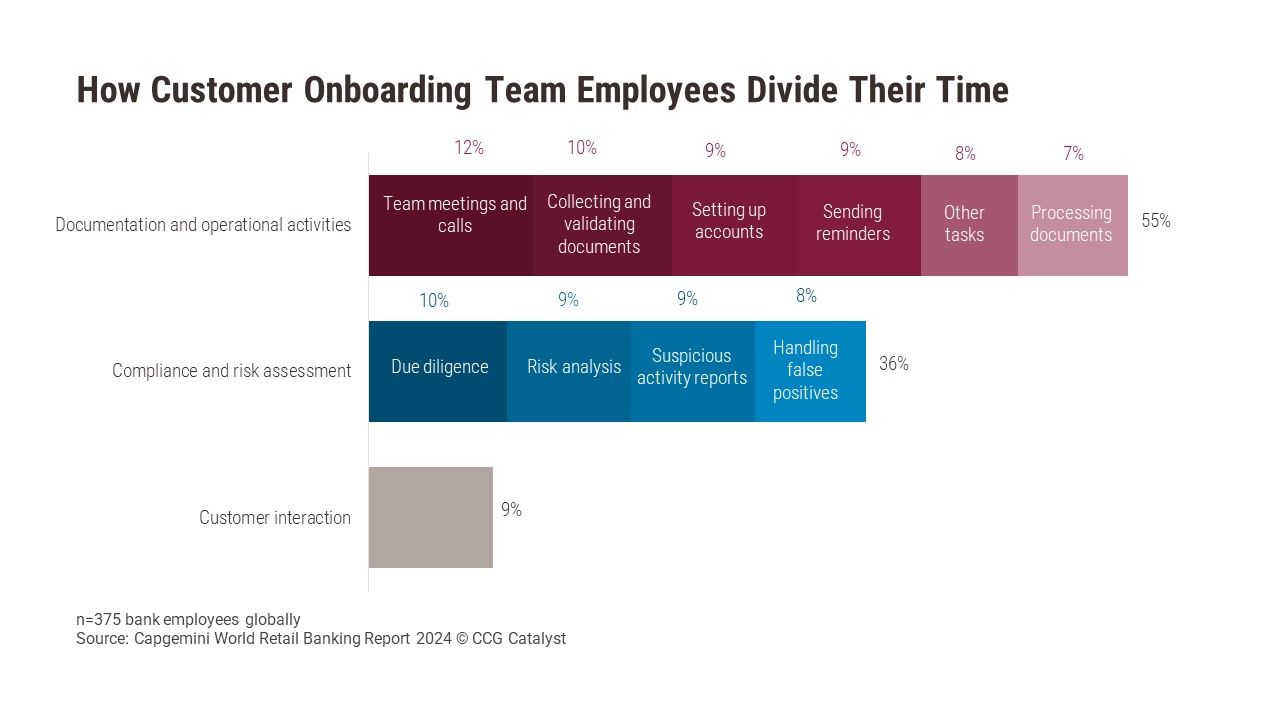

Documentation and operational activities take up 55% of customer onboarding teams’ time, according to Capgemini’s World Retail Banking Report 2024. Most of the rest — 36% — is related to compliance and risk assessment-related tasks. Banks face both costs and lost revenue associated with long and cumbersome onboarding processes. On one side is the cost of employees’ time, and on the other is the risk of losing a customer. Capgemini estimates the cost of onboarding a customer totals $128, on average, and per the report, there’s an 18% customer abandonment rate.

Many banks have responded to the need for digital onboarding capabilities, but the process can still be tedious for employees and customers: Time employees spend on onboarding tasks adds to the time a customer waits for an application decision. According to Capgemini’s data, just 4% of customers globally opening accounts get same-day approval. Another 34% are approved in up to 5 days, and 44% are approved in between 6 and 10 days. For the rest, it takes even longer. The 18% of applicants who give up while they’re waiting erases potential long-term business for the bank.

Shrinking the amount of time onboarding employees spend on tasks that they can automate, potentially with help from artificial intelligence (AI), reduces the bank’s costs related to onboarding and lowers friction for consumers. Lower friction, crucially, reduces the probability that a customer abandons an application. Advances in AI-driven identity verification,in particular have made the process easier for customers, more accurate, and therefore more likely to expedite onboarding.

Modern ID verification goes beyond an ID document’s text to recognize document security features, like microprints and holograms, and check for tampering or manipulation of the document. It may add another layer of security by building biometrics into the verification process. For example, the ID verification flow may try to match a photo on an ID document to an applicant’s selfie or do a “liveness check” to assure that the applicant is a real person and the same one who is applying. It may also use contextual clues, like location of the applicant vs. their legal address, to “step up” the verification process.

The Holy Grail of account opening is a straight-through, real-time onboarding process — cutting the human component from the moment a customer starts an application to when they get a decision and delivering that decision in seconds. AI-driven onboarding solutions, especially those that automate mundane, repeatable steps, are a promising step toward making that a more common reality. As banks contemplate their next moves in onboarding, they should look to work with providers embracing these capabilities.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.