How Wallets and Banks Could Partner on Travel Spending

How Wallets and Banks Could Partner on Travel Spending

March 7, 2024

By: Tyler Brown

Credit Cards and Rewards

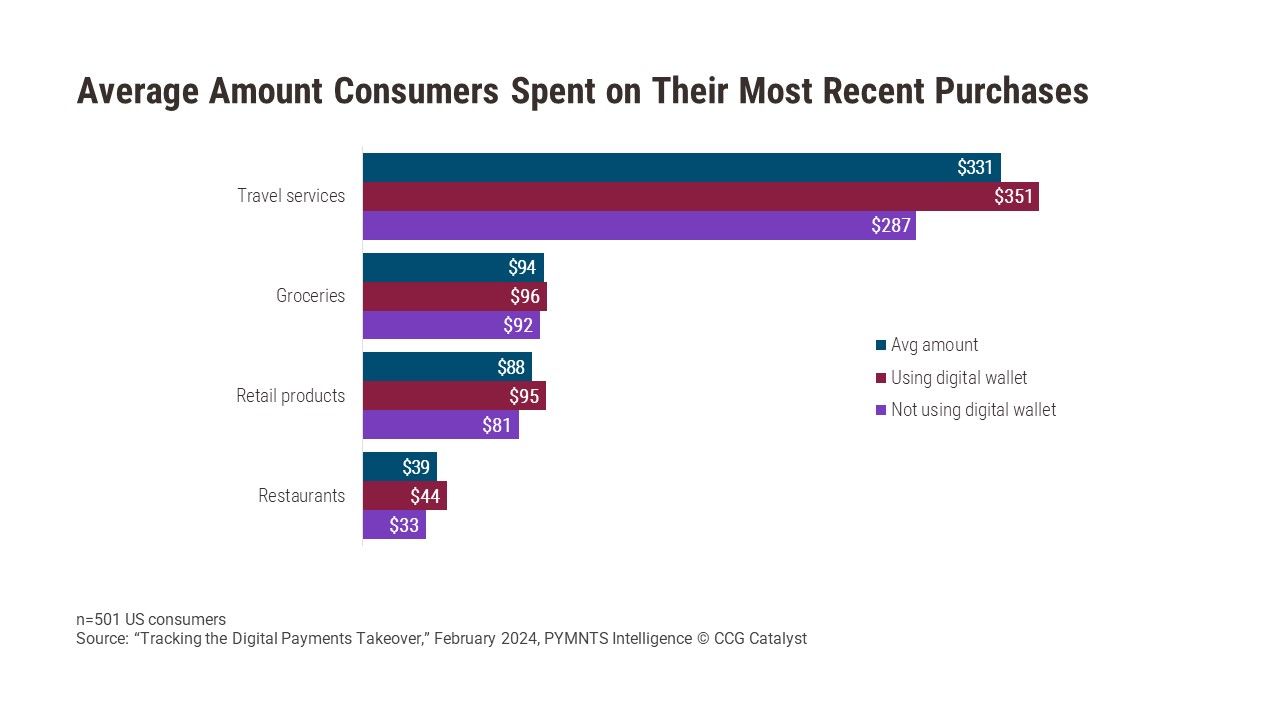

Travel expenses are, on average, high relative to expenses for groceries, retail, and restaurants, according to a survey by PYMNTS Intelligence. The average size for consumers’ most recent travel purchase was $331, eclipsing the three other categories by hundreds of dollars. That’s not a surprise — the “travel services” category covers leisure travel, which can include pricey items like hotels and plane tickets. In 2023, airplane tickets averaged about $427 for a domestic round-trip ticket, according to Forbes Advisor, and several nights at a mid-range hotel could cost more than $500.

Credit card issuers want a piece of those high-dollar transactions and go to great lengths to acquire and engage customers that make them. In particular, travel rewards and perks are a core benefit of many high-end credit cards, like those offered by American Express, Chase, and Capital One. However, the PYMNTS data flags an opportunity that traditional loyalty programs don’t address: the possibilities of digital wallets. Per the report, the average travel services transaction size for consumers who used a digital wallet was $64 higher than for consumers who did not. This offers potential upside for travel-related credit cards that are tightly coupled with digital wallet offerings and could be a strategic consideration for any issuer with affluent or affluent-to-be customers.

The tendency to spend more through digital wallets may be for several reasons, including the ease of using embedded payments at online checkout, the convenience of having a payment method already stored, the security of not using a card number, or the integration of card-related or wallet-offered discounts or rewards. That last one speaks to how credit card issuers (and wallet providers) can capitalize on this spend, because if a user can see and spend their rewards from within their wallet app, that can help build loyalty with the card issuer as well as the wallet provider. This gives issuers and wallet providers an incentive to work together to craft such experiences.

Overall, big travel expenses are valuable for credit card issuers and digital wallets alike, and, on average, consumers’ transactions tend to be larger when they use a wallet. As such, both players stand to benefit when they partner in ways that enhance customer loyalty. Embedded rewards are the most obvious example today. In practice, this amounts to issuers collaborating with wallet providers like Apple Pay, Google Wallet, and PayPal to enable access to their own rewards portals, perhaps first through read-only permissions that let users see rewards balances but eventually extending to the ability to book travel, hotels, or even redeem points for cash — all from within their wallet app.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.