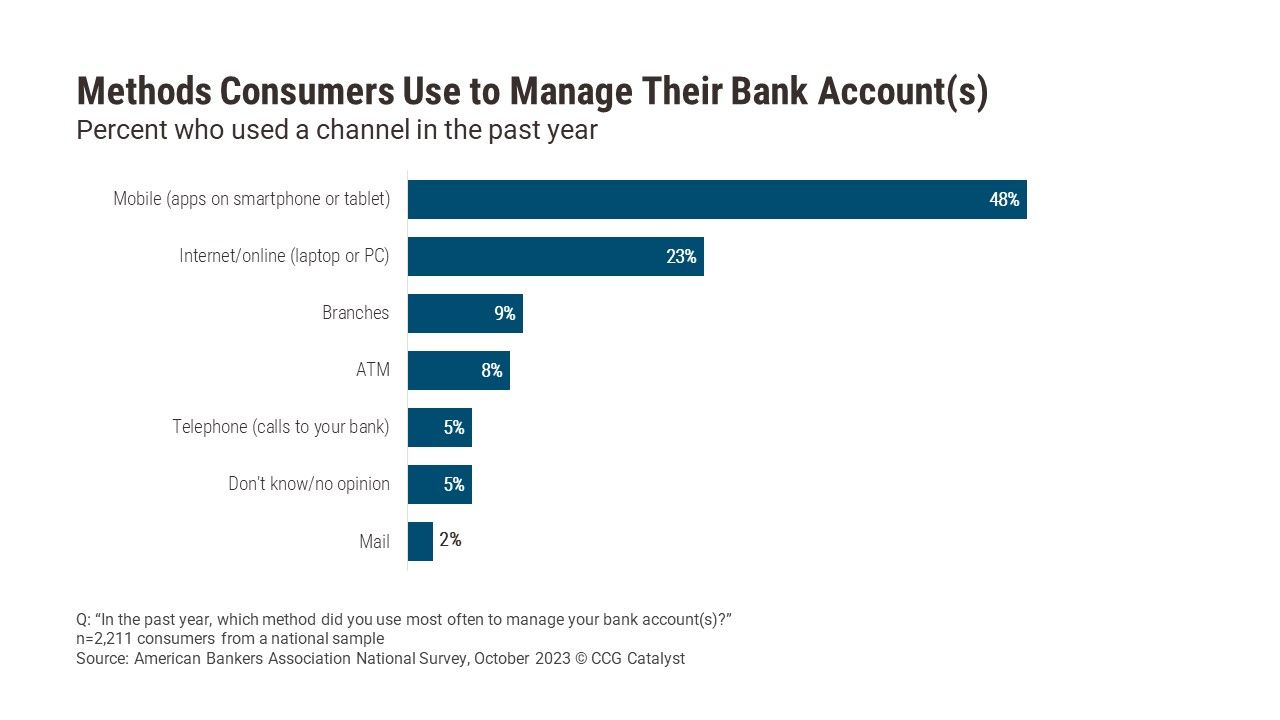

The difference between the number of consumers who use the online vs. mobile channel to manage their bank account(s) is stark, according to a study by the American Bankers Association. Twenty-five percentage points more consumers used mobile than online, and that difference rose to 46 percentage points for both millennials and Gen Zers.

The 46-point gap should remind bankers how crucial mobile banking is to attract, retain, and engage consumers aged 18 and 43 — a cohort that gets more earning power every day. A retail bank can’t afford to do without a mobile app that manages basic financial products like checking accounts and credit cards. Beyond that, more sophisticated functionality is important as younger consumers’ finances grow more complex.

Banks need a channel strategy that anticipates these consumers’ behaviors, expectations, and needs over time and in any context. The dominance of mobile highlights three initial investment priorities:

Apps. Today’s menu-driven mobile banking apps are increasingly rich in features, and bankers shouldn’t skimp on functionality. Achieving a competitive set can be a long road, but it’s also the baseline for the next generation of tools. Tomorrow’s apps may, for example, have artificial intelligence-driven experiences that respond to user behavior and replace menus with dynamic suggestions.

Two priorities go beyond the bank’s app:

Platform integration. Smartphones create a natural payments experience using features built into the device and the operating system. The bank doesn’t control that experience. But by making its products compatible with a platform’s features, like a mobile wallet, the bank can be the preferred payment choice and stay top of wallet when a consumer uses the device for a transaction.

Omnichannel journeys. Mobile can complement rather than compete with physical channels. The use of offline channels for managing a bank account is low, but the branch and ATM are ancillary services. Basic omnichannel may be as simple as offering ATMs that work with the phone’s tap-to-pay feature instead of a card.

As we wrote last week, consumer demand gives banks a strong incentive to invest in the customer experience. Mobile is just part of it. Banks naturally should offer an app and take advantage of smartphone features, but a truly modern approach goes beyond that. Serving customers well in the long run depends on the real-time integration of services across a bank’s products, including customer data held in different siloes.

A bank’s goal should be to have holistic customer data in real time to support responsive, relevant experiences. Few tech stacks are well-equipped to overcome data siloes, and putting off that problem means falling behind. Gradual migration is a likely solution, but it’s a very long journey that takes strong commitment from the board and senior management.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.