Payment Services May Be the Real Fintech Threat to Banks

March 14, 2024

By: Tyler Brown

Payments Fintechs and Banking Competition

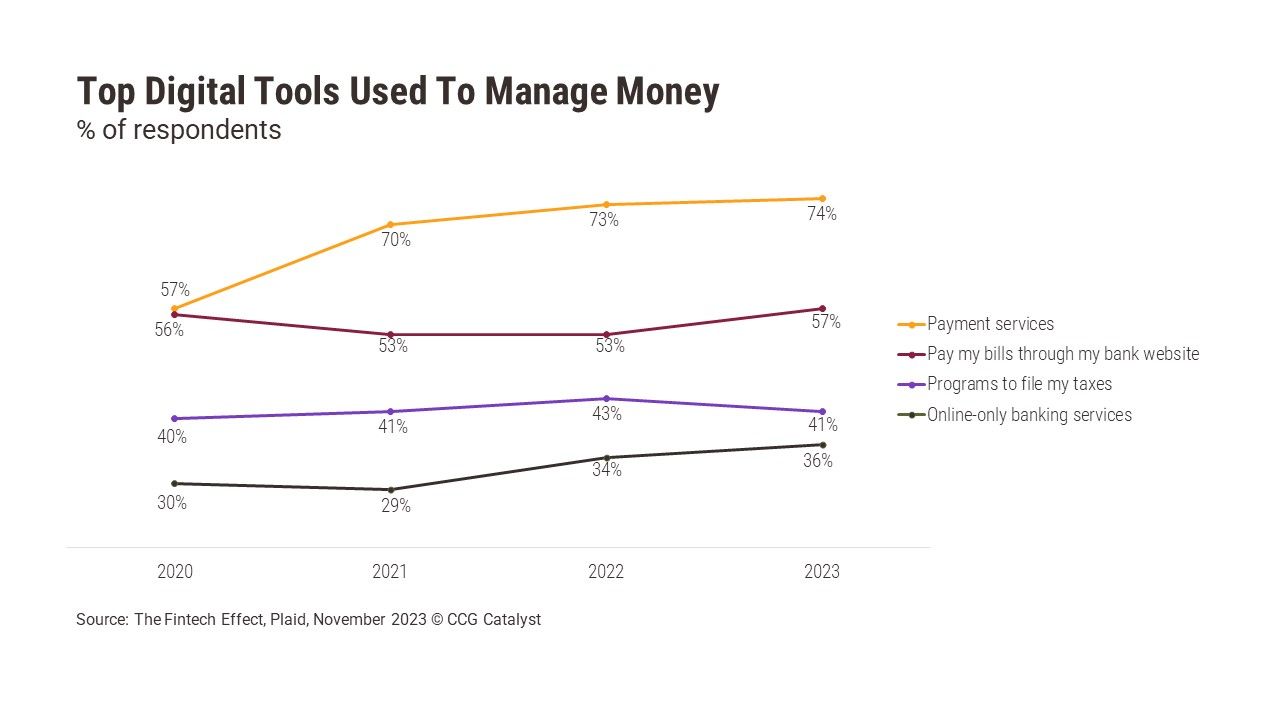

Payment services are the most popular digital tools to manage money, used by 74% of consumers in 2023, according to a survey commissioned by Plaid. That’s a rise of 17 percentage points since 2020. US peer-to-peer payment (P2P) apps — like Cash App from Block and Venmo from PayPal — counted about 158.1 million users in 2023, suggests an EMARKETER forecast, and P2P transaction volume was forecast to grow to $1.26 trillion. That’s in sharp contrast to stagnation in online banking and bill pay in the survey.

Consumer’s stagnant use of these legacy banking services between 2020 and 2023 and growth in payment services points to a competitive threat to banks. They haven’t been left out entirely — Zelle users were about 43% of US P2P users in 2023. But banks play second fiddle to tech companies in the mobile wallet space, which was forecast to count 114.8 million users last year. Banks may feel the urge to retreat from innovation in the wake of regulatory scrutiny of the fintech sector, but this data should remind them that established payments fintechs and big tech companies continue to grow their influence.

Block, for example, recently laid out its ambitions in banking. According to its latest shareholder letter, it plans to turn Cash App, its consumer app, into “one of the top providers to households in the US which earn up to $150,000 per year.” Much of the app’s roadmap should be familiar to digital bankers: Features planned include enhanced customer service, spending insights, subscription management, and credit building. Block also aims to integrate buy now, pay later (BNPL) features via its acquisition of Afterpay and tie the Cash App ecosystem of consumers with the Square ecosystem of sellers.

Big tech companies, meanwhile, have both partnered with banks for wallet services and encroached on them with financial products. Apple has gotten ahead of banks with BNPL and supports a P2P feature in its messaging app. Google continues to iterate on its wallet, although it’s shutting down its Google Pay P2P service in the US. PayPal, which markets both a digital wallet and a mature P2P service as core offerings, enables consumers to pay with a variety of payment methods including its own.

These companies boast immense financial firepower, making them a credible long-term threat. Neobanks, which styled themselves as competition to banks, have faded out of view. PayPal, for example, reported $26.9 billion in transaction revenue for 2023. Block reported Cash App transaction-based revenue of $498.2 million in 2023, augmented by subscription- and service-based revenue of $4.7 billion. Apple, with 2023 revenue of about $383 billion, and Google, with 2023 revenue of $307.4 billion, aren’t short of funds to compete with the banking industry however they choose to.

Banks may be able to coexist with payment services if they effectively address two factors. The first is to operate on the right platform. Mobile is key — in the past year, consumers most often used mobile banking to manage their bank accounts, according to an American Bankers Association Survey, including 57% of Gen Zers. The second factor is to support the right features. The banking industry successfully addressed P2P with Zelle and may do the same with wallets using Paze. But as challengers make further inroads into financial services, to thrive, banks must commit to a strategic vision, the thoughtful and ongoing deployment of new features, and the right partnership strategy to develop them. They shouldn’t be caught playing catch-up with app features like spending insights, subscription management, or credit building. They should also constantly reevaluate their competitive positioning and how well they serve their target demographics.