Sector Spotlight: Business Banking Platforms

May 13, 2025

By: Tyler Brown

Business banking platforms can support a range of financial operations for financial institutions’ business clients. They fundamentally enable businesses to manage balances and move money. But the scope and sophistication of features, which may range from fundamental account management and payments tools to sophisticated treasury functions, can differ dramatically by platform and target market. The larger and more complex the target customer, the more advanced the tools:

What’s going on in business banking platforms

Many business digital banking platforms have grown to integrate more or more advanced cash management and treasury features and sell to financial institutions with larger, more sophisticated commercial clients. Some treasury management features have trickled down to solutions for smaller commercial clients, while treasury management workstations remain purpose-built products that are exclusive to corporate banking.

Below are four key trends and considerations for banks and credit unions, incorporating current developments in the business banking platform sector, keeping in mind different types of solutions:

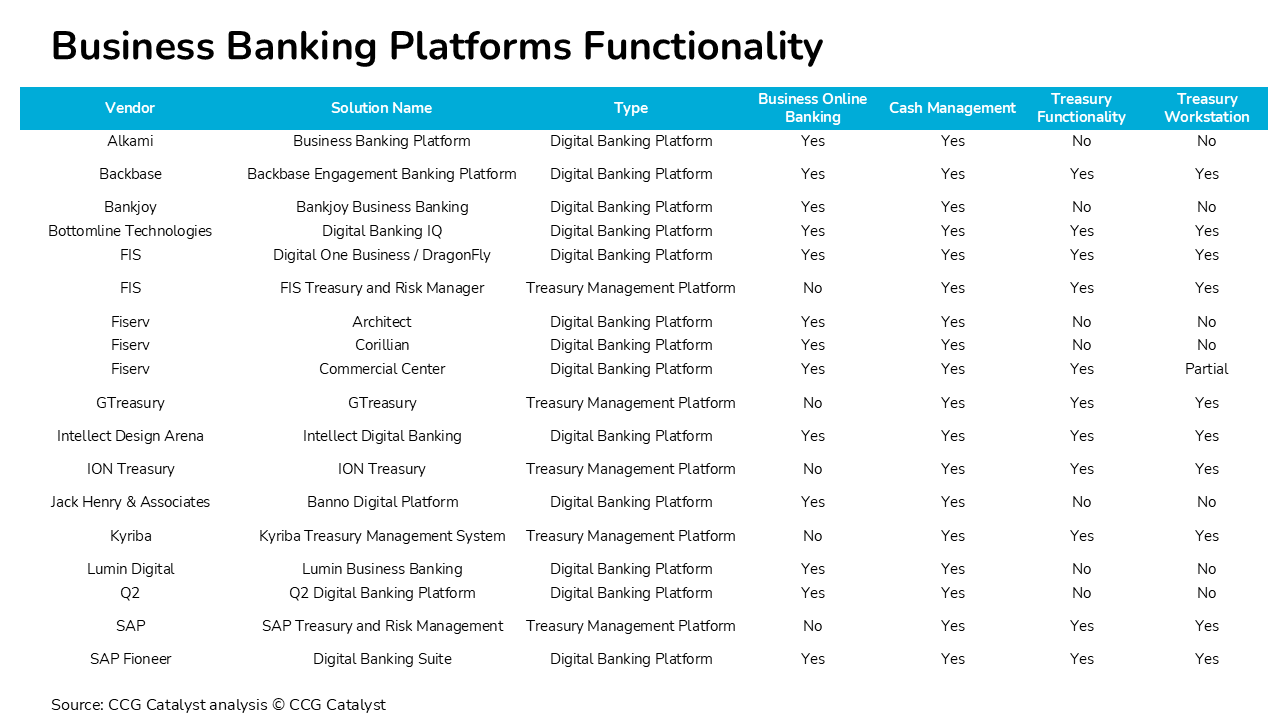

Business banking platform vendor snapshot

The business banking platform space is complex and, while features may overlap, solutions are designed for specific customer segments and the types of financial institutions that serve those segments. A bank or credit union’s choice of business banking platform will depend on its business and functional requirements.

Here’s a snapshot of business banking platforms. The list is representative:

What to look for in business banking platforms

Features to look for in business banking platforms depend on the segments financial institutions serve. Features aren’t mutually exclusive between customer groups; more sophisticated platforms built into digital banking may incorporate components of simpler software and vice versa, but treasury workstations are a different animal.

SMB (i.e., fundamental self-service with tools for businesses):

Large commercial/corporate (i.e., complex treasury management):