Sector Spotlight: Real-Time Payments

May 27, 2025

By: Tyler Brown

Real-time payments are account-to-account transactions initiated by consumers and businesses that are irreversible and settle within seconds via networks that operate 24 hours per day every day of the year. In the US, those networks are the Federal Reserve’s FedNow and the Clearing House’s (TCH’s) Real-Time Payments Network (RTP).

Real-time payments are distinct from faster payments, such as same-day ACH, which have a shorter settlement window than three-day ACH, or like Zelle, which may appear to the customer to be in real time, but the money may not move for hours or days.

What’s going on in real-time payments

RTP has been live for 8 years, and financial institutions rapidly adopted FedNow after its launch in 2023 (although RTP and FedNow adoption are still both below 20%). Currently, few institutions have qualms about receiving real-time payments, but many are concerned about how unauthorized push payment fraud may lead to losses from sent payments. Meanwhile, the “request for payment” capability could make real-time payments more useful by allowing merchants and billers to request payment from their customers, or consumers from each other, but it isn’t top of mind. Choices may also depend on an institution’s payment processor. The Fed, for example, most recently had 40 FedNow certified service providers, all of which offered receive-only capability, 38 of which offered send and receive, and 16 offered the ability to receive a request for payment.

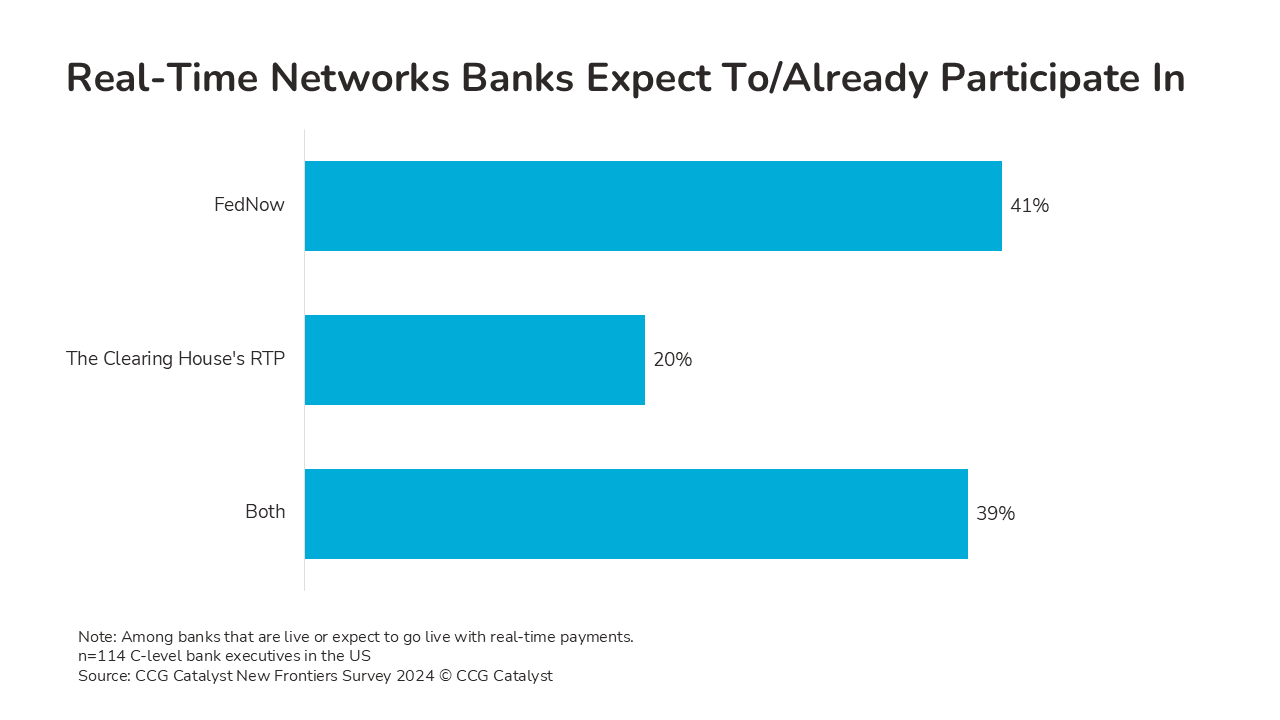

Real-time payments network snapshot

As US banks contemplate their payments strategies in the context of real-time payments, which network to start with and perhaps to operate exclusively is a key decision. In our research, there isn’t a consensus. In our New Frontiers Survey 2024, among banks that are live or expect to go live with a real-time payments network, 41% said they are or would be FedNow participants. Twenty percent said so for RTP, and 39% said both.

When an institution chooses to go live with either FedNow or RTP, its decision may depend on its attitudes about network ownership, the benefits of network scale, transaction size needs, desired settlement mechanism, and cost to operate. It isn’t an either-or decision, but institutions may choose to prioritize one based on their preferences and customers’ needs. In broad strokes, RTP is the private-sector solution with higher transaction limits and has been most suitable for institutions that handle large corporate instant payments. FedNow is the public alternative that caters to all US institutions.

Here’s how FedNow and RTP compare:

Ownership and access

Network size and composition

Payment purpose

Operations

Cost

What to look for in a real-time payments network

The networks’ features and day-to-day functions are similar, and as FedNow matures, obvious factors like network-mandated transaction size limits are becoming less of a differentiator. A network’s attractiveness and features to enable will ultimately depend on business needs and other participants’ characteristics: