The Risk Open Banking Payments May Pose to Banks

May 2, 2024

By: Tyler Brown

Instant Payments and Credit Card Issuers

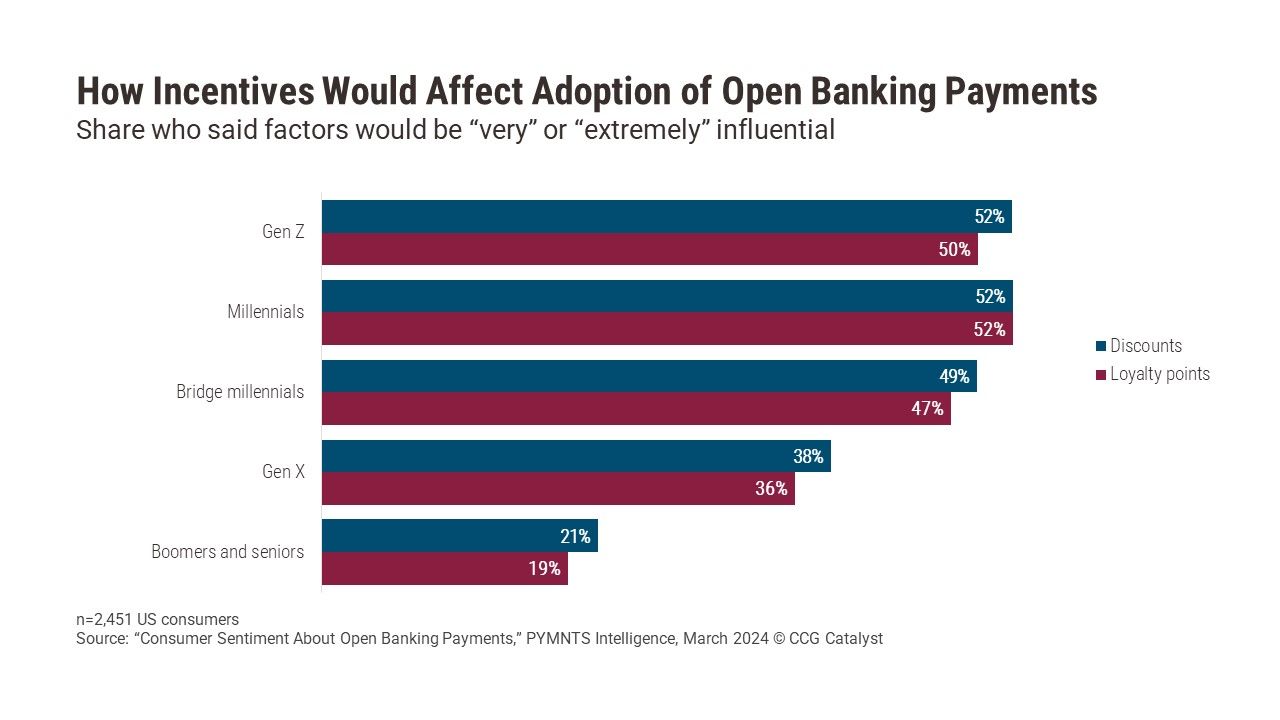

Discounts and loyalty points would be very or extremely influential to the decision that 50% or more of Gen Zers and millennials might make about their adoption of open banking payments, according to a PYMNTS Intelligence study. Consumers’ willingness to use open banking-facilitated payment is becoming increasingly important: Financial institutions (FIs) and payments processors across the US have been going live with FedNow, the Consumer Financial Protection Bureau’s (CFPB’s) final rule on open banking is due this fall, and both Visa and Mastercard now operate open banking divisions in the United States.

The instant payments and open banking trends could mean that account-to-account (A2A) transactions directly challenge FIs’ credit card issuing businesses and compete with debit cards for share of wallet: Open banking payments could cut into the profits issuing banks earn on credit cards and disrupt the checking account-based banking relationship that debit cards support. FIs may also be forced to cede share of the customer relationship to apps with open banking payments capabilities, and unforeseen competitors, if they don’t keep a close eye on the threat.

The number of potential players in open banking-facilitated payments makes it complicated to keep track of competitors and partners. FIs, aggregators, card networks, payments processors, merchants, and consumers are all part of the evolving dynamic. The most important players banks should focus on today are themselves, merchants, and consumers — all key to how open banking-facilitated payments might affect revenue from interchange, interest, and fees.

If open banking-facilitated payments were to take off, merchants would probably be happy. They may need to pay for updated terminals and software, but with FedNow’s per-transaction tariffs of $0.01 or less, fees charged to merchants would almost certainly be much lower than the percentage-of-transaction fees dictated by the card networks. With instant A2A payments, they also wouldn’t have to wait to be paid by their acquiring bank.

FIs, however, would probably not be pleased. The cost burden of instant payments and open banking APIs would fall on them, and if open banking payments displaced credit cards, issuing banks would need to find sources of replacement revenue for cards. This may also be an issue for acquiring banks — they would likely have less float related to card payments. Little, in theory, would stop issuing banks from compensating for card revenue with overdrafts and per-transaction fees, but regulators might get in the way.

FIs can take heart for now that consumer habits will slow down open banking-facilitated payments as a competitor to cards in retail spending. Consumers are very attached to cards and would need reasons to care much more about using open banking-facilitated A2A payments to switch — including rewards programs that beat credit cards, meaningful discounts, and a better day-to-day payment experience, as the PYMNTS data illustrates.

It’s a huge hill to climb for merchants to successfully push consumer adoption of open banking-facilitated payments. For now, FIs don’t need to worry much about lost revenue from open banking payments, but they need to be vigilant and have regular strategic conversations about the changing payments landscape. If A2A payments catch on with consumers, the challenge won’t be a simple one to fix.

We just published our report “US Open Banking 2024,” which covers the history of consumer financial data-sharing in the US, the CFPB open banking rule’s implications for how consumers access their financial data, compliance challenges for FIs, and the industry’s way forward.

Click here to read the key findings and download a free copy.