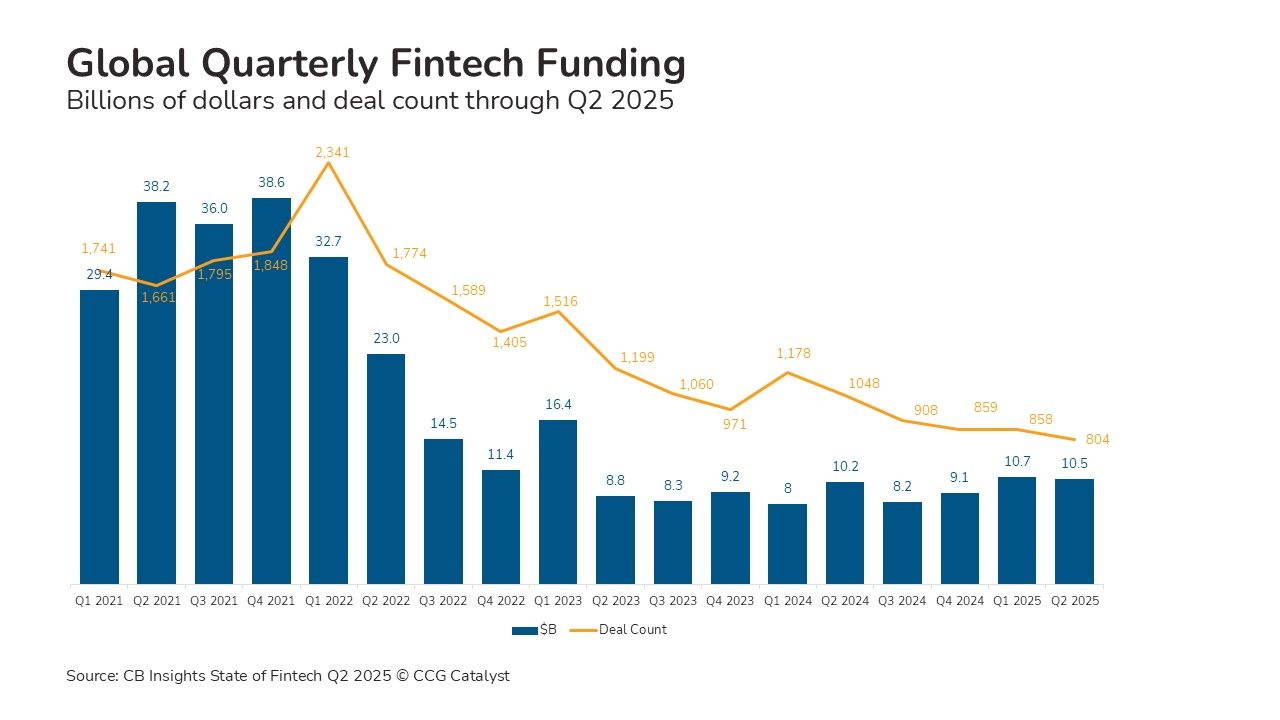

Funding to fewer companies, even as capital increases, is part of a broader theme we’ve been tracking for a while by which rounds are getting bigger, and investors are getting more selective. It reflects a separation of the wheat from the chaff. This is good news for traditional financial institutions (FIs) that are interested in working with fintech companies and leveraging their innovations, because it suggests the fintech industry is getting stronger, and therefore less risky to engage with.

Moreover, the amount of funding flowing to business-to-business (B2B) companies, which includes those selling into FIs rather than trying to compete with them, remains healthy. Here are a few examples from the latest quarter:

Plaid ($575 million round): Love it or hate it, the data aggregator is a force to be reckoned with on the US open banking scene. The company is known for providing the plumbing that allows fintech companies to connect to consumers’ banking apps. However, it also supports traditional FIs through services like digital identity verification, instant account verification, streamlined account funding, and data analytics.

Persona ($200 million Series D): Persona is a verified identity platform based in California and founded in 2018. It provides a suite of identity services to customers in and outside of financial services, including KYC/AML and KYB. Persona is especially known for its focus on managing identity in an evolving fraud environment, characterized by AI-powered bad actors. It counts OpenAI, Square (Block), and Heritage Bank as customers.

Thunes ($150 million Series D): Thunes is a cross-border payments infrastructure player, based in Singapore and currently expanding to the US. Its Direct Global Network enables real-time payments across 130+ countries, 80+ currencies, and 550+ direct integrations. It also has a partnership with stablecoin issuer Circle that allows members of the network to facilitate transactions using USDC.

As we move forward, we expect the fintech industry to continue to produce innovative companies solving real problems for banks, with less focus on consumer fintechs like neobanks that aim to compete. “Fintechs are eating banks’ lunch” is no longer the phrase du jour. As such, the next wave of fintech may well be far more supportive of the traditional financial services ecosystem than the last. Banks and credit unions would do well to keep an eye on these developments — the fintech industry still matters, but in a different way. A shift from threat to opportunity may be on the horizon.