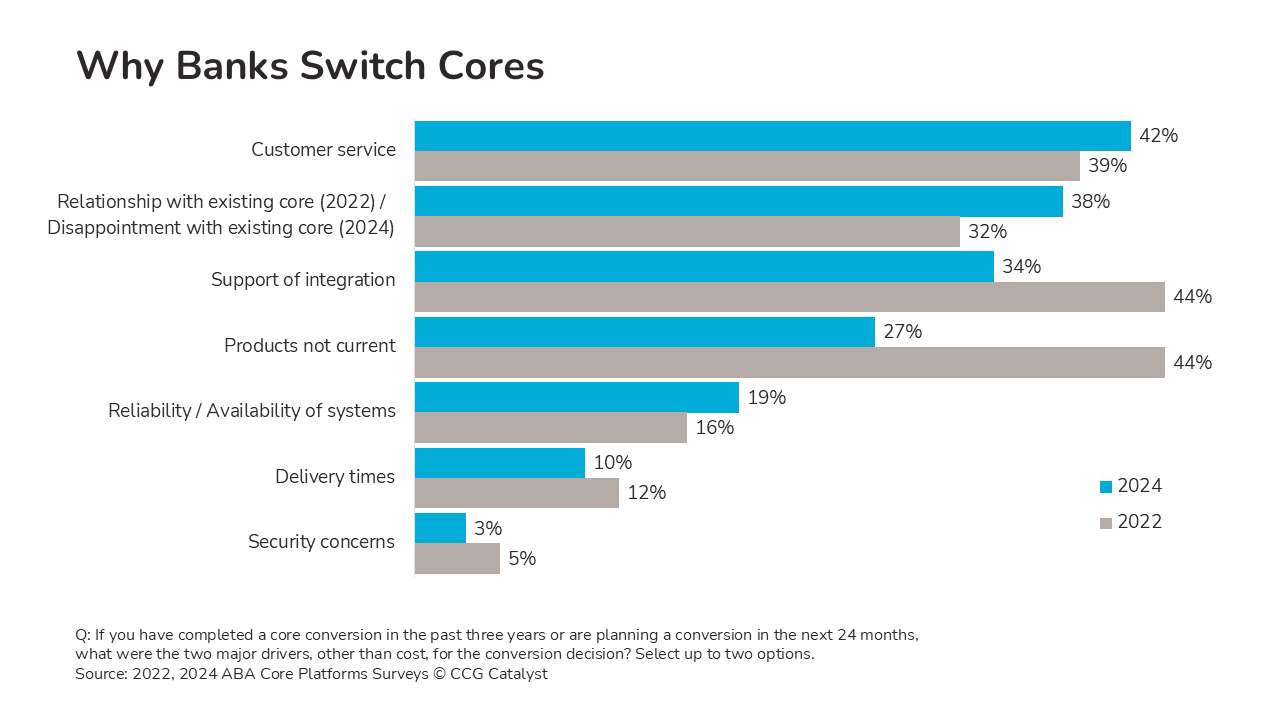

The top reason banks complete core conversions is customer service, according to the ABA’s 2024 Core Platforms Survey. While not unsurprising, this does mark a major departure from 2022 when the top two reasons were support for integration and products not current. This shift says a lot about the market and where we are today.

Let’s take a stroll down memory lane. What was it like in 2022? Well, that was before the bank collapses of March 2023. And, while the market was showing signs of a slowdown from 2021, things hadn’t hit the fan yet. It’s likely those survey results reflect a generally positive attitude toward innovation and desire to move forward. In particular, the need to for greater integration support points to a fintech fervor at the time, when everyone was high on open banking, Banking-as-a-Service (BaaS), and the possibilities of plug and play.

Things have clearly changed. In fact, when was the last time you heard anyone talk about plug and play with any real enthusiasm? The 2024 data suggests that bankers have truly gone back to the basics, and the ones leaving their core providers now are not those frustrated by their capabilities but those who feel the relationship has soured. This is the innovation pendulum in the wild. (To be fair, this data is from 2024, but aside from chatter about AI and stablecoins, things feel similarly today; innovation still doesn’t seem to be getting the same level of attention or urgency it once had.)

Meanwhile, technology hasn’t advanced so fast in the last few years that core systems no longer have capability shortfalls. Many legacy cores still struggle to integrate and stay current with new technologies. So, a reasonable explanation for the latest results is that bank leaders don’t care about those things as much, or at least not enough to make a change. This is deeply, deeply disappointing. Technological advancement should not be a fad; it should be a pillar of a carefully crafted and future-driven strategy.

As core contracts come up for renewal, banks should take on this challenge: Formally review your strategy, review your core’s capabilities, and map them to each other. Make sure that the bank’s technology can support its future vision. Don’t assume it does, and don’t go off a gut check. Take the time to assess whether you’ve got what you need for the future. Even if it turns out that the bank’s current system is suitable, this work can help uncover areas and asks that will be important in renegotiating with your existing provider.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.