I’ve seen community banks grapple with core system modernization throughout my long career as a banker and a consultant. These conversations are often somber, filled with fears of disruption, betrayal by vendors, and the daunting cost of change. Yet, in a world where fintechs and neobanks are redefining banking, modernization is no longer optional. Community banks face a triple threat: outdated systems, unreliable vendors, and fierce competition. The good news? Community banks can evolve without risking it all.

The problem: a broken partnership

The core vendor-banker relationship is often like a marriage entered without really knowing the other person. You discover your partner doesn’t listen. It’s hard to compromise; they don’t understand your problems, nor do they take the time to do so. You might find your core vendor touts their “partnership” credentials, while their solutions feel like they were designed in a vacuum. And, because of how agreements are structured, divorce is hard.

A major issue is that many vendors lack firsthand banking experience. They’ve never managed a balance sheet or faced a regulator’s scrutiny. The only CAMELS they know are animals. This leaves them out of touch with bankers’ realities. Their modernization attempts — shiny dashboards, a consolidation of two or more first generation cores into a new core that is still a first generation core, or touting cloud-based add-ons — prioritize sales over substance. When banks call for help, they are met with understaffed support teams or boilerplate responses. One banker told me recently their bank waited months for a vendor to fix a critical reporting issue, only to receive a half-baked workaround.

Bankers, meanwhile, dread the risks of modernization. A failed core conversion could mean downtime, lost customers, or regulatory penalties — existential threats for banks with razor-thin margins and a limited IT staff that’s often just one or two people juggling everything from cybersecurity to ATMs. Add to that the competitive pressure from fintechs, and it’s clear why many bankers feel trapped.

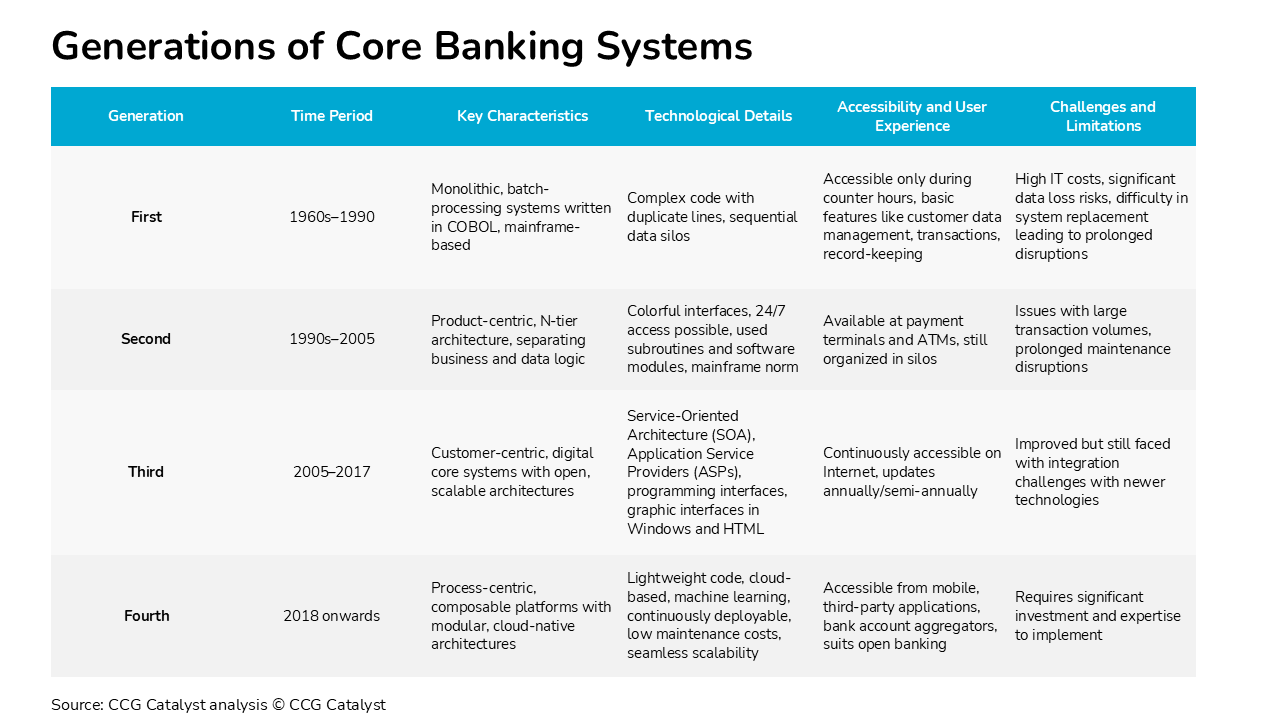

Understanding core systems

Before we can have a conversation about what to do, we first need to understand the core system landscape. I’ve written about this extensively here. Most community banks rely on legacy core systems, each with its strengths and limitations:

Switching cores is daunting. Multi-year vendor contracts and proprietary data formats make it feel like rewriting the bank’s DNA. A typical conversion costs hundreds of thousands to millions, halts other initiatives, and demands extensive staff training and data migration. For small banks, it’s like climbing Mount Everest in flip-flops. Understanding what you have and what is out there is a good first step in making the process more palatable.

Assessing your core

If your bank is running a first generation core, it’s likely a reliable workhorse — your ledger is rock-solid, and it gets the job done. But is it the right system, and is your vendor the right partner? Before deciding to stay or switch, ask these critical questions:

If your first generation core aligns with your strategy, has reliable vendor support, and keeps you competitive, staying put may be wise. But if it’s a mismatch — or your vendor’s promises fall flat — consider switching to a better-fitting first generation or second generation system. This isn’t about chasing the latest tech; it’s about ensuring your core serves your bank’s unique needs.

A path forward: smart modernization

The assessment phase will help your bank determine whether your current system is meeting your bank’s needs and where the gaps are. In the end, it may require a core system swap, it may not. But it’s important to remember that, even if you decide to stay with your current system, modernization is still an imperative. There are a couple of ways banks can approach this shrewdly and strategically:

These strategies aren’t pipe dreams — they’re happening now. Banks that adopt them are staying competitive while minimizing disruption.

The risks of inaction

Sticking with a “if it ain’t broke, don’t fix it” mindset may feel safe, but it’s a losing strategy if your core can’t keep up. Legacy systems, even the best first generation cores, struggle with customer expectations. Fintechs and neobanks, unburdened by old technology, are stealing market share with innovative, customer-friendly solutions. Standing still cedes ground to competitors and risks long-term irrelevance.

Community banks have survived wars, recessions, and fintech invasions — they can survive this. But survival demands action. Assess your core, reject complacency, and stop waiting for vendors to lead the way. Explore incremental upgrades, collaborate with peers, and hold vendors accountable. Your customers, shareholders, and community are counting on you. Roll up your sleeves — the future belongs to banks that act.