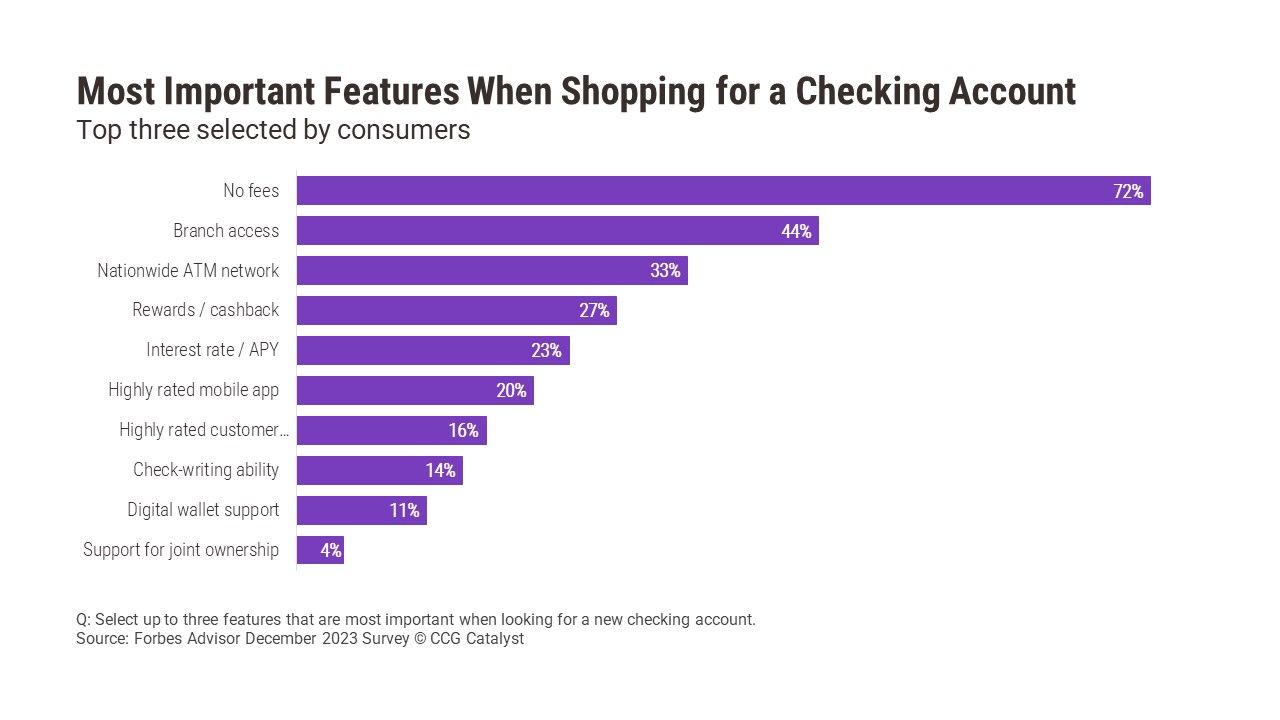

Consumers are clear about what’s most important to them when they’re opening a checking account: Over 70% selected “no fees” as a top-three feature when shopping for a new checking account, according to a survey by Forbes Advisor, making it by far the top choice selected. But what consumers want and need from a checking relationship goes beyond product features to channels — “branch access” is the second-most important feature, followed by a “nationwide ATM network.”

Bankers should think of channels as customer acquisition (as well as engagement) tools and remember that brick-and-mortar plays a big part. Channels’ value as an incentive to prospective customers depends on how prospects envision their interactions with a bank’s products and services. Some channels — the branch and call center in particular — are also a safety net for when self-service isn’t enough or for when customers need detailed advice, even for demographics less likely to use them generally.

It can be easy to forget about the value in physical touchpoints as digital becomes the primary channel for customer interaction. As we recently wrote, nearly half of US consumers used mobile banking the most in the past year to manage their account(s), followed by nearly a quarter who used online banking to do the same. But even when a bank’s customer base leans increasingly toward digital, physical channels can be a powerful secondary option and should get appropriate attention and investment.

When bankers plan how channels and products will be used to attract new customers, they can break down demand into two categories: demand for the products and services customers are buying and demand for modes of access. Some product features have immediate, tangible benefits that can be strong motivators in a buying decision. Examples include fees, high interest rates, and no minimum balances. Ways to access those account features matter as much, if not more, but their benefits may become clear over time, post-acquisition, at the engagement stage.

Bankers should ask themselves how they’ll demonstrate upfront the value of channels most customers won’t use day-to-day. Then, they need to invest appropriately. Cost minimization should never be the answer — letting legacy channels follow inertia or consciously picking the cheapest options are lapses in good management and strategic planning. The operative word is optimization: making physical channels attractive, efficient sources of revenue that fit into omnichannel journeys.

The successful use of physical channels for acquisition and engagement requires a deep understanding of what prospects want and how customers interact with a bank’s touchpoints. Bankers need to do market research, gather appropriate third-party data, and map out an analytics strategy that gives them a holistic understanding of customer and noncustomer needs, wants, and intentions. As part of long-term planning, bankers should pay constant attention to how physical channels fit into what consumers demand in an increasingly digital world and shape a brick-and-mortar strategy accordingly.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.