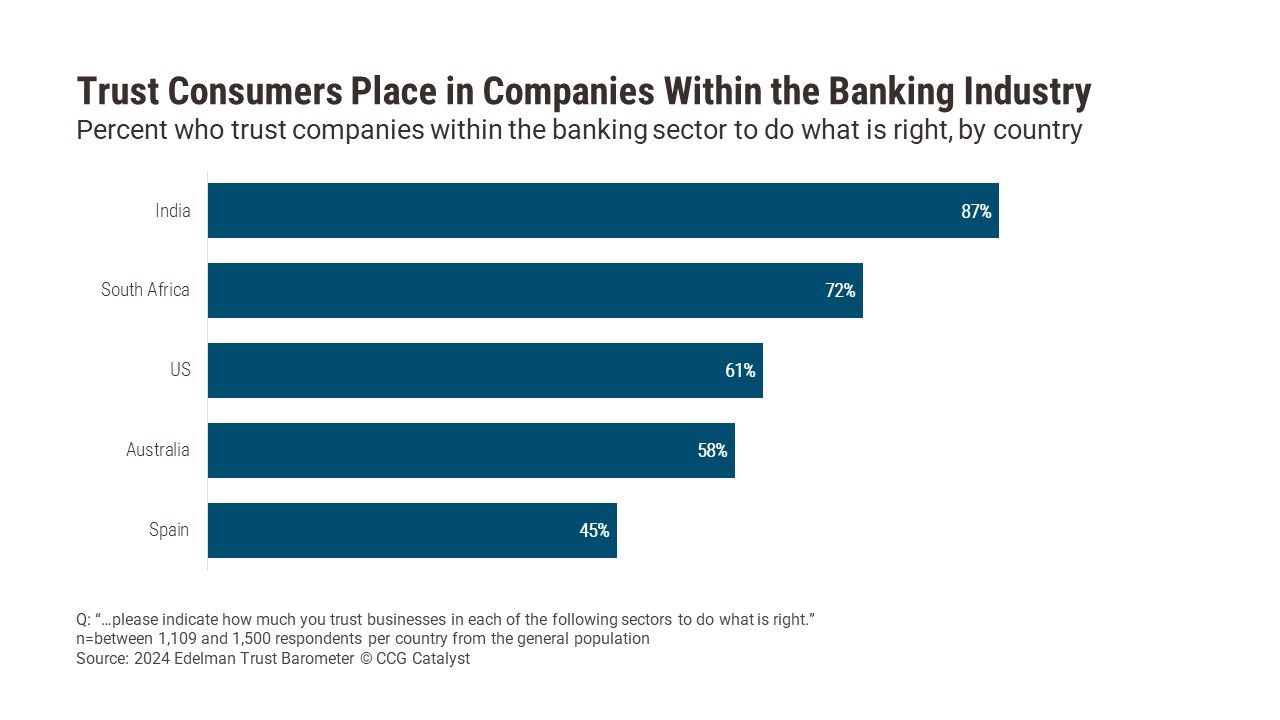

US consumers narrowly trust companies in the banking sector to do what’s right, according to a survey by Edelman. The 61% of consumers who rated it as trustworthy put the sector in Edelman’s “Trust” range of 60-100%. India was at the top, with 87% of respondents who said they trust the banking industry, and Spain was at the low end, with 45% who said the same. The US numbers hardly changed year over year, falling by two percentage points, suggesting a measure of stability.

That stability may come as a surprise given the survey’s timing. It was fielded in November, less than a year after the high-profile failures of Silicon Valley Bank, Signature Bank, and First Republic Bank; two other bank failures; the closure of Silvergate; and the sale of PacWest. Financial institutions (FIs) should take from these numbers that consumers’ trust in the US banking system is tenuous but can quickly snap back. With the right investments in customer relationships and a consistent projection of stability, FIs should retain their customers’ trust in the long run and be prepared to weather short-term turmoil.

Crises, however, can dent relationships no matter the trust in the system and test the strength of the customer bond. As we wrote in April, the acute stage of the 2023 banking crisis shook consumers’ confidence in the stability of their bank. The bank runs were terrifying for FIs because little could be done to stop them, particularly amid poor preparation. The lesson should be that customer confidence in the FI can drop without warning, and an improvised response may not be quick enough.

FIs need a framework for customer retention that stands in even the most difficult times. Based on our research, there are two main parts to this:

Long-term trust building. FIs should shape a brand identity around a reputation for stability and transparency. That includes responsible balance sheet management and a marketing strategy that engages customers and sets a baseline for stickiness.

Crisis preparation. FIs should plan how to respond to a crisis. Crises may be specific to the bank, like with a data breach, or caused by the industry at large, like with a large-scale liquidity crunch.

Bankers may get lucky and never have to ride out a storm, or if they do, have the tumult pass quickly and without impact. But it pays to prepare. It’s dangerous for an FI to find itself in the middle of a crisis without a plan, particularly when that crisis could destabilize the institution. It’s crucial that FIs cement a trusting relationship with customers during normal times, giving them a cushion when customers get nervous, and be able to act swiftly and with confidence when there’s a risk of panic.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.