What Stands Out in Fintech’s Doldrums

April 25, 2024

By: Tyler Brown

Banking and Venture Capital

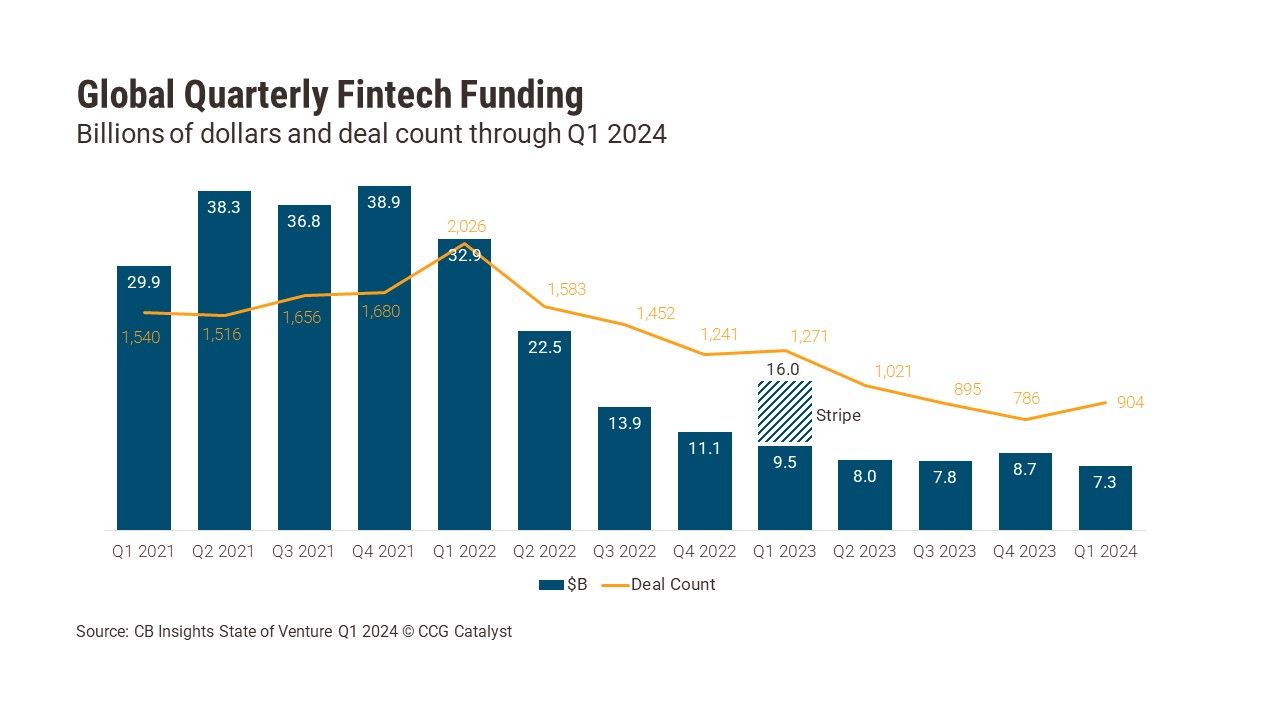

Fintech funding fell again in Q1 2024, according to CB Insights, with $7.3 billion in global capital raised across 904 deals. However, it isn’t all bad news: While the rebound we’ve been waiting for hasn’t arrived, narrower activity stands out. We continued to observe relative strength in B2B fintech and also saw unexpected activity on the consumer side.

Specifically, the quarter’s biggest deal was for Monzo, which raised a Series I worth $431 million. Monzo is a UK digital bank, and it’s had a remarkable recovery from a difficult 2021, which led it to turn a monthly profit for the first time in 2023. The company’s initial push into the US was largely lackluster, but with this fresh funding, such expansion is reportedly back on the table. Monzo today is a sort of incumbent in the UK, and with fewer neobank competitors in the US, it may see success if it competes effectively with both incumbents and the increasingly concentrated consumer fintech market.

As we’ve written, retail banking fintech offerings with the best prospects come from a handful of payments providers and tech companies. Monzo’s product line sounds like what Block has planned Cash App — mobile banking features that match legacy banks with basic utilities, wrapped within a comprehensive and compelling experience that most banks would struggle to offer. Monzo UK offers features that include open banking-enabled account management, subscription management, spending categorization and budgeting, fee-free cash reloads, and fee-free withdrawals abroad.

On the other hand, all but one of the six other big Q1 deals identified by CB Insights were in the B2B space. And even with the market’s excitement over artificial intelligence (AI), the top fintech equity deals included only one with a fintech branded as an AI company. Here are some highlights of the names that raised money in Q1:

Despite the muted environment — high-profile fintech layoffs we wrote about last quarter are still a bit fresh, and quarterly global fintech funding just hit its lowest point in more than four years — bankers must keep an eye on the themes that attract investors’ attention and money. In Q1, those included both direct competition from retail banks (Monzo), and new applications for banking (Kore.ai). The fintech threat is present but mostly quiet, and technology is emerging to help banks better address it.