Banks Lag on Serving Younger Customers

December 8, 2021

By: Kate Drew

Banking Younger Generations

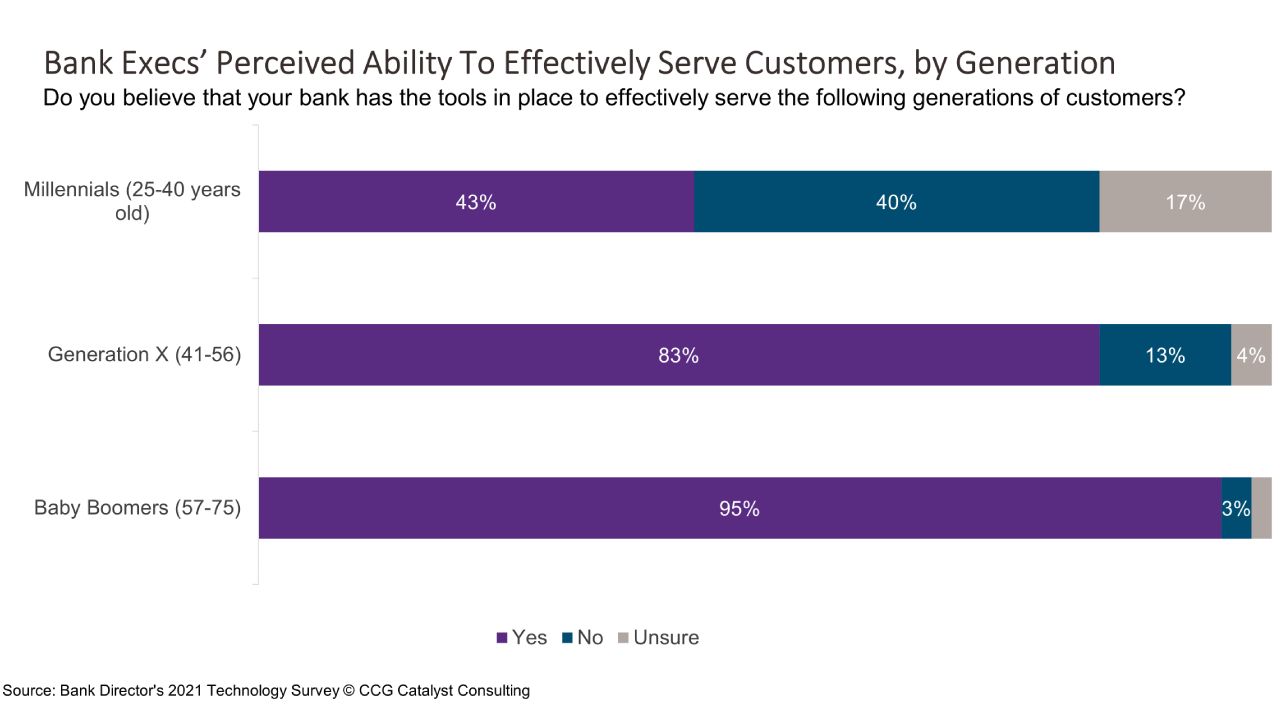

Banks in the US are unprepared to serve younger generations — and, they say so. According to Bank Director’s 2021 Technology Survey, just 43% of respondents feel their bank has the tools in place to serve millennials (dubbed those 25-40 by the report), compared with 83% and 95% for Gen X (41-56) and Baby Boomers (57-75), respectively. This data is concerning because the millennial generation is growing increasingly important over time — as the report notes, older millennials are reaching 40, signaling that they are beginning to take leadership roles in the workforce and build more wealth. In fact, the millennial cohort is expected to increase its earning power by almost 75% in the next couple of years, according to The Economist.

Adding to the conundrum is that this generation doesn’t seem to stick around the way previous groups have — according to another study by Capco, 53% of millennial respondents said they switched banks at some point in the past two years. As we’ve highlighted before, this is likely in large part because younger consumers tend to be the most courted by digital challengers and neobanks that bring to market slick experiences designed to delight their users. Neobank Current, for example, which boasts over 3 million users, has an average customer age of 27. The tendency of these customers to jump ship to these newer, tech-savvy players, coupled with banks’ own admittance that they feel behind in catering to such users, suggests there is little time to waste in getting prepared to serve them. Moreover, while we may be talking about millennials right now, Gen Z is coming up quickly and joining the workforce with its own set of needs, putting even more pressure on banks to figure out how to satisfy emerging generations.

We’ve been beating this drum for a while, but it is well deserved: Getting to these consumers is going to require a commitment to user research and testing. That’s how neobanks are pulling them in — by taking time to understand their needs and then delivering on those needs. Digital is just the delivery mechanism. Younger generations are complex and nuanced; they grew up with Uber at their fingertips and Amazon at their doors. It’s going to take work to understand them. Perhaps the reason banks feel so comfortable serving Baby Boomers isn’t so much because of “the right tools” but because they understand them more. They’ve had decades to get to know their needs and desires. The problem today is that nascent customer groups aren’t going to wait around for banks to figure them out. They move fast, and you will have to, too. That’s where research and testing come in. So, make the first move and get to know them. Talk with them, survey them. Become acquainted before it’s too late.